Cote d'Ivoire is among Africa's fastest growing economies. After years of political instability, key political and economic reforms have improved security and bolstered the country’s economic resilience, helped by a strong energy sector and a National Development Plan that focuses on inclusive growth. Cote d'Ivoire has maintained a strong economy and a high GDP growth rate since 2012 that has reduced poverty levels from 51% in 2011 to 46% in 2015 (The World Bank).

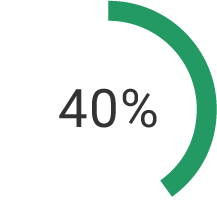

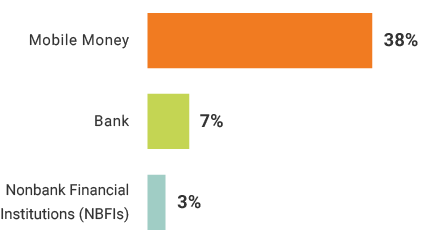

According to the FII 2017 survey, 40% of adults were financially included in Cote d'Ivoire. Mobile money is the main driver of financial inclusion unlike some other West African countries, such as Ghana and Nigeria, which rely heavily on banks. Mobile financial services were introduced in 2008, and major mobile operators like Orange Money and MTN Mobile Money dominate the market. Adoption of mobile money has increased rapidly, boosted by government and private sector partnerships for implementing e-payment systems. In 2017, 38% of the adult population (ages 15+) had a registered mobile money account. Banks are much less popular than mobile money; only 7% of the population reported owning a registered bank account. The banks have started to compete with mobile network operators by developing mobile banking apps, mobile wallets, and online-only banking systems.

A common barrier to access and adoption of any formal financial institution is a lack of digital skills and financial literacy. As Cote d'Ivoire's economy is poised to continue growing quickly in the coming years (projected annual growth rate of 7.6%), a key part of the country’s financial inclusion initiative will be to bridge the digital and financial literacy gap among the unbanked and unregistered users.

Financial Inclusion

Mobile Money Use

Mobile Credit

True or false

In 2017, 41% of adults had never sent or received a text message.

What percentage of adults held registered bank accounts in 2017?

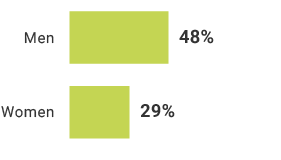

What percentage of females own a mobile phone in Cote d'Ivoire?

True or false

In 2017, only 40% of adults were financially included.