Bangladesh Bangladesh leads FII Asian countries’ mobile money usage, although most transactions are conducted through unregistered accounts.

Benin While Benin has a low overall financial inclusion rate, there exists a sizable portion of the population that possesses the readiness factors.

Côte d’Ivoire As one of Africa's fastest growing economies, Ivorians are becoming more and more financially included through mobile money.

Ghana In Ghana, the digital financial services (DFS) sector grew from an estimated 150,000 active users in 2011 to more than 4 million in 2015.

India Between 2014 and 2018, the proportion of the financially included population grew from 54% to 81%. Bank accounts are the main driver of financial inclusion.

Indonesia With the highest income per capita among the 8 FII countries, Indonesia promises great potential for financial inclusion—26% of adults are financially included.

Myanmar Despite going through enormous political and economic transformations in the last decade, Myanmar has relatively high levels of literacy and digital skills to be able to adopt DFS in the future.

Nigeria As Africa’s largest economy, Nigeria has potential to drive consumers toward financial inclusion, yet internal strife and economic instability make progress uncertain.

Pakistan With more than 180 million adults but only 1 in 10 (9%) financially included, Pakistan is one of the largest unbanked countries in the world.

Rwanda Mobile money services were introduced in Rwanda in 2010, and their use has grown tremendously (1 in 4 Rwandans now use the services).

Senegal Senegal has the lowest rate of formal financial account ownership of all African FII/MM4P countries.

Tanzania Five in 10 Tanzanians (54%) are currently financially included, mainly through mobile money accounts (53%).

Uganda Mobile money is leading the way to Ugandan financial inclusion, and 4 in 10 adults (40%) have financial services accounts.

Agriculture Agriculture is the bedrock of many of FII countries’ economy; yet agricultural workers tend to be poorer, less financially included, and older than other workers.

Banking Banking plays a key role in India, Indonesia and Nigeria’s move toward financial inclusion. In Bangladesh and East African countries, mobile money is testing bank relevance.

Financial Literacy The foundation for financial literacy, basic numeracy, paves the road to financial inclusion.

Gender Women lag men in the use of financial tools across every measure, and closing the gender gap requires motivating women to adopt financial mechanisms.

Mobile Money Using a simple mobile phone to conduct financial transactions has help bring financial inclusion to millions of consumers in the developing world.

Mobile Phones Research shows the most effective way to significantly expand lower-income populations’ access to formal financial services is through mobile phones.

Nonbank Financial Institutions Nonbank financial institutions (NBFIs) vary from country to country by provider type, service option, and marketplace presence.

Over-the-Counter Many consumers first interact with digital financial services by reaching out to mobile money agents to help send or receive money through an OTC transaction.

Youth Digitally more active yet financially less secure, youth (ages 15-24) are a particularly important segment to target for financial inclusion.

Economic Empowerment FII found that being financially included is associated with an increase in economic empowerment, but the increase is smaller for women versus men.

Financial Health While the gains seen vary by country, on average, financial health increases with greater education.

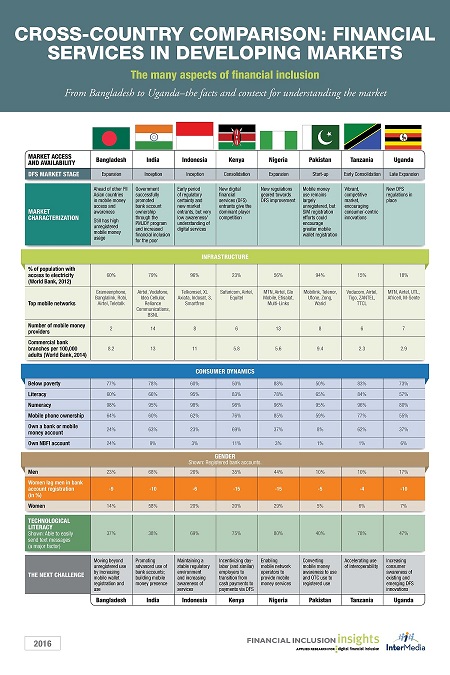

Cross-Country Comparison: Financial Services in Developing Markets Jun 3 2016 The many aspects of financial inclusion